Whether you want a loan to pay off a debt, make an emergency payment, or simply spend on something exotic, getting a personal loan can be easy, quick, and cheap. These are the top 10 best personal loan companies I tested and ranked:

- Credible – Best overall

- LendingTree – Best for comparing loans

- Fiona – Best for low credit

- Upgrade – Best for covering large expenses

- Marcus – Best for flexibility

- LoansUnder36 – Best for competitive rates

- 5KFUNDS – Best for quick funds

- Monevo – Best for loans with great terms

- SoFi – Best for debt consolidation

- AmOne – Best for a wide range of loan amounts

1. Credible

Credible gives borrowers a chance to review rates from different lenders in only 2 minutes. This can be done in a way that won’t affect your credit score. Just input a loan amount in the range of $1,000 to $100,000 and enter some details about what you need.

Details such as the loan purpose, your current level of education, employment status, estimated earnings and credit score, your name and date of birth.

These details will help to get you a personalized rate, not a ballpark figure. The better your credit, the more your rates will be better, making Credible one of the best personal loan companies out there.

Credible also rates its lenders, giving you rates from about 11 lenders for debt repayment, or what it calls “loans for life,” like moving costs, weddings, vacations, and other financial goals. You’ll see the loans you qualify for, complete your application online, and also close your loan. Once you’ve signed the documents, relax.

The money will be sent to your account. Credible has an “excellent” (5 star) rating on Trustpilot and offers lenders for almost any financial need, which includes debt repayment, credit card refinancing, home renovation, bad credit loans, private student loans, and student loan refinancing.

With a client success team that’s always eager to assist and is only a call, email, or chat away, Credible can assuredly call itself one of the best personal loan providers on the market.

Pros

- They have zero fees

- Provides low APRs

- Very fast in responding

- They have huge range of loan amounts

Cons

- They require higher credit scores

- Does not give credit

2. LendingTree

LendingTree is really one of the best personal loan companies in the industry. This company is a wonderful loan marketplace, advertising only 3 steps you can take to your best loan.

The first step is to answer a few questions about the type of loan you want and how you intend to use it. Then they’ll submit your request to its vast lender network. In no time, you’ll see lenders offering competing options for your business.

Next, you’ll review and go through the offers, looking at loan terms, interest rates, and any other terms, conditions, or additional fees. There are zero fees from LendingTree itself, and no markup on your loan.

You can review offers side-by-side, speak with loan officers from individual lenders, or just apply online with one simple application.

There are lots of educational resources too, so you can know your credit score. You can also calculate your estimated monthly payments and understand more about loan vocabulary and the know-how.

LendingTree even has its own mobile application, with which you can know your credit score. It can also give improvements, and be on the lookout for other lower rates for your personal loan options.

Pros

- Provides a large marketplace with a range of loans

- They charge no fees for connecting you with lenders

- Has excellent educational resources

Cons

- You’ll be contacted by too many companies

- They do not get more involved than matching you with lenders

3. AmOne

This company is always there to provide you with a free and easy way to find your best loan options. It’s a loan marketplace with an efficient process, targeted loan options for you, friendly customer service, and at zero cost. Their customer support is US-based, and the loan providers are highly recommended and secure.

It works in a similar fashion to other loan marketplaces: you’ll provide some basic information, such as the reason for the loan, your financial information, and how much money you want. The best options will then be selected for you so you can get approved quickly, giving it a place on the list of the best personal loan companies.

They also have personal loans, debt repayment, and credit card consolidation loans, as well as loans for business startups. They have live loan experts that are always available by phone, so you can know which loan you need easily.

If your credit isn’t excellent, that’s okay too, because you can get a bad credit personal loan or credit card through AmOne too.

Pros

- They have a large range of loan terms and amounts

- Huge network of lenders

Cons

- Has very few customer support channels

- They’re not upfront about rates and terms

4. Upgrade

All the personal loans gotten through Upgrade have APRs of 6.94%–35.97%. Their personal loans have a 2.9%–8% origination fee, which is subtracted from the loan proceeds. This is why Upgrade is one of the best personal loan companies to go for.

The lowest rates need Autopay and the paying off of a portion of an existing debt directly. The APR on your loan may be higher or lower and your loan offers may not have several term lengths present.

The real rate depends on your credit score, credit usage history, loan term, and other things. Late payments or subsequent charges and fees may make the cost of your fixed-rate loan to be higher. There are zero fees or penalties for repaying your loan early. All personal loans are given by Upgrade’s lending partners.

You can get updates on Upgrade’s lending partners can be found here.

Pros

- They have a quick online application process

- You can get a pre-approval in minutes

- They have a credit health tracker

Cons

- They require a 6% origination fee

- All the applicants are required to have $1,000 cash flow

5. SoFi

They’re known as one of the best community lenders and also one of the best personal loan companies. This is because SoFi has a comfortable borrowing experience, and it really tries all it can to break the idea of the ruthless, corporate, financial institution that wants to take the consumers for everything they’ve got.

Instead, SoFi has removed all fees, and it includes borrower-friendly terms, and even offers social networking events for its community members. Yes, SoFi is definitely breaking a lot of set ideas about lenders.

However, does SoFi cope well against the competition when it comes to personal loans? To start with, SoFi offers APRs that are as low as 5.99% (using AutoPay).

This is a good amount, but what’s really amazing about these loans is that they come totally free. There is no origination, no closing fees, no-prepayment penalties, and not even late fees, which truly makes this one of the most appealing options for anyone on a low budget.

Pros

- They charge absolutely no fees

- SoFi offers high loan amounts

- It’s a good way to protect against unemployment

Cons

- Not good for people with poor credit

- They’re not available in the state of Mississippi

6. Marcus

This platform by Goldman Sachs is a good lender. It has an excellent financial backbone, so it doesn’t need to employ tactics that other less reputable and less stable lenders sometimes employ. Essentially, Marcus is one of the best personal loan companies and also a lender you can trust.

Additionally, because this lender calls its own shots, you can expect some refreshing flexibility from your loan terms. For instance, Marcus gives borrowers a chance to set their own loan terms when applying for their loans.

That’s correct, you can select how much you want to pay each month or the duration of your loan. This is an innovative way of approaching lending, and it’s a wonderful change for most borrowers.

Pros

- You can choose monthly amount and loan terms

- They have free financial tools online

- You can defer payment option

Cons

- You can’t sign up with a cosigner

- They’re not available in all states

7. 5kFunds

Getting the money you need is relatively easy with 5kFunds. You can start by filling out the simple, secure, online form. It doesn’t matter what your credit history is, this form can help you get a lender that works best for the loan you need.

Once you’ve picked a lender and been approved, the money will be sent right into your bank account, without any checks or trips to the bank.

5kFunds services are always totally free of charge, but some lenders might charge fees (and interest). Every lender is expected to provide you with full disclosure of their loan terms once you’re approved. You’ll only get quotes from credible lenders or lending companies who are authorized to lend cash in installment loans.

All you have to do is to submit your required loan amount, name, zip code, and email and you’ll begin the process of getting the funds you want.

Pros

- They have a US-based customer service

- You’ll get matched instantly with a lender

- They have an easy application process

Cons

- You can borrow only up to $35,000

- They have very few educational resources

8. Monevo

This is definitely Europe’s largest personal loan marketplace and platform, which offers an award-winning service that enables you to browse over 30 top lenders and banks. You can receive personalized offers in 60 seconds with no credit impact, and super low rates.

The company also enables you to get a great rate on a loan from many of the best lenders with no obligation or fee.

Monevo’s smart technology gives your details to lending partners to know if there are loan offers based on your personal details. In just a few seconds, you’ll get offers from lenders. When you’re ready to proceed with an offer, you’ll click “continue,” with no commitment.

The service is totally free and there’s no obligation to move forward once you get a rate quote, and it has no impact on your credit score.

Loan providers will send you decisions fast, so you can know what your offers will be right away. This is why I added it to my list of the best personal loan companies.

Pros

- They have a transparent comparison table

- Has an easy, step-by-step application

- Provides a fast service

Cons

- They don’t have a FAQs section

- Having a lot of options can be overwhelming

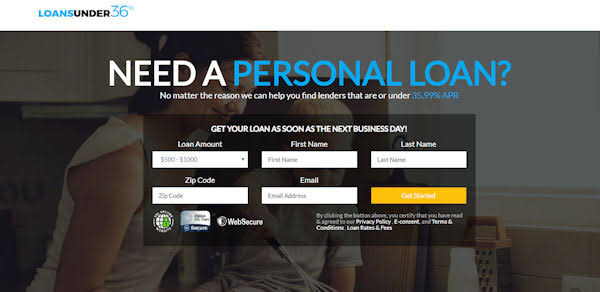

9. LoansUnder36

This is one of the best personal loan companies in the US and for good reason. With this platform, you can receive your loan possibly the next business day, without leaving your home.

The online form is fast, secure, and hitch-free, and all types of credit can get a loan offer. Get the funds into your account very quickly, and get a real solution that works for you.

They work really hard to make sure that all borrowers are treated equally and with transparency and have a high standard of customer service. You can take a loan from the range of $1,000 and $35,000, and rates are guaranteed to be no higher than 35.99%.

There are also flexible short-term loans and multi-year terms available too, making this a flexible partner in your personal loan goal. You’re free to use the money to do whatever you want to do.

Pros

- They have a single application for multiple lenders

- Provides a large lender network

- Has a strong customer support

Cons

- They have a small range of loan amounts

- Not a direct lender

- Their website is sparse with information

10. Fiona

This company is a personal loans marketplace that can assist you in saving both time and money. You can filter loan offers by credit rating (the higher the better), zip code, the purpose of the loan, and the amount of loan, and pick from the top offers given almost instantly.

You’ll get paired with personalized offers in about 60 seconds from top lenders. Then you have to choose the offer with terms you agree to.

If approved, you’ll get the money in your account right away. It’s very safe and super secure with 256-bit encryption, a higher standard of security than many banks. Thus, giving it a spot on the list of the best personal loan companies.

Pros

- They have only one application for many lenders

- You’ll have no negative impact on your credit score

Cons

- You’ll get lots of offers

- They have a limited number of lenders

Frequently Asked Questions

1. Is getting a personal loan worth it?

Personal loans can be an immense help for people who need a huge amount of money for projects. Are you in dire need of money for an emergency project or you want to make timely payments? Then taking a loan with one of the best personal loan companies is worth considering as it is a good option for tackling financial hurdles.

2. How adversely does a personal loan affect your credit?

A personal loan can badly affect your credit score if you don’t repay on time. Due to the effect of interest and fees, a personal loan can also spike your debt credit, adding more of a strain on your personal finances. However, if you repay your loan on time, you can maintain and even strengthen your credit score.

3. What is the best reason I can give when applying for a personal loan?

You can take a personal loan for a variety of reasons, and usually, the reason of the loan is less important for a personal loan than other loan types. The usual reasons for taking out personal loans are medical costs, rents, and bill payments.

4. What things do you need to know about online personal loans?

Any person who has had any form of cash flow problem, or encountered an emergency, or need funds to pay for medical expenses, home improvements or even a college education has most probably thought about a personal loan.

Personal loans are good because they give you the chance to acquire large investments and pursue future goals. However, there are various kinds of loans and it’s crucial to know your needs and financial condition before deciding on which type of personal loan is best for you.

5. How did I rate the best personal loan companies?

I took my time to review all the most popular providers based on factors such as:

- Loan amounts

- Rates

- Fees

- Loan terms

- Customer service

Of course, there are a lot of things to consider when getting the right loan, one of the most important things is finding a credible, trustworthy lender from the list of top personal loan providers.

A credible lender will provide you with a loan that suits your needs, walk you through the application and repayment processes, and be transparent and upfront about their fees and charges.

6. How do I apply for a loan with a reliable lender?

In order to get a reliable lender, first of all, make your research so that you can find a reliable personal lender. These are the things you have to do to get ready to apply for a personal loan so you can discover the best personal loan provider for your needs.

Calculate the amount you need to borrow

When you’re taking a personal loan, you might be tempted to borrow a bit more than you need. It’s necessary to bear in mind that you’ll be repaying every dollar that you borrow, so even an extra $100 could end up costing you much more in interest. A reliable lender will not advise you to borrow more than necessary.

On the other hand, you don’t want to borrow too little and discover that you don’t have enough to cover the purchase you wanted to make.

Make Your Research on Loan Providers

Make proper research and compare reviews about the top loan provider for your current situation. Bear in mind that the best loan provider for your next-door neighbor might not be the best for you, even if they are a trustworthy lender. Below are some things to take note of in your research:

- Look for loan providers that cater to borrowers with your credit score. If your credit score is bad, find lenders that specialize in bad credit loans

- Focus on your reasons for the loan. Some loan providers may have restrictions on your loan purpose

- Whether you want fixed or variable payments

- Whether or not you need a secured or an unsecured personal loan

- The duration of the repayment term—do you need a long-term loan, a short-term loan, or a micro-loan for just a few months

- Whether you can borrow the amount you want as different lenders have different minimum and maximum loan amounts

- Whether you can get customer support if you need to suspend payments for a short period

In addition to getting the best lender for your needs, there are important factors to look for that show a credible lender that you can trust. For a start, do not work with a lender that isn’t approved by a regulatory body and obeys all national financial laws. When you’re picking an online loan provider, you have to also take note of customer reviews.

Of course, there will be the odd negative review, however, if the majority of the reviews are unhappy with the lender, or you see the same complaints appearing, again and again, be warned. Lastly, every responsible online lender should be highly security conscious when it comes to the application and payment process.

Check your credit score

When you’re going for a personal loan, your credit score is the most important factor. Your credit score dictates whether you’ll get lower interest rates if you’ll be eligible for special financing deals, and whether or not you’ll qualify for a personal loan at all. A credible lender runs a credit check to confirm that you can repay your loan.

Credit scores generally appear like this:

- Excellent: 720+

- Good: 690-719

- Fair or Average: 630-689

- Poor: 300-629

If your credit rating is average or poor, you may want to take some time to improve your credit score so that you can apply again and be eligible for better loan terms.

Find out your debt-to-income ratio

The other important factor in being eligible for a personal loan is your debt-to-income ratio. This translates to how much debt you carry in relation to your income.

To calculate your debt-to-income ratio:

- You have to add up all of your total monthly debt payments, including mortgage debt, credit card debt, and student loan debt

- Next, add up your total monthly income, such as your paycheck, dividends, or income from real estate

- Then divide your total monthly debt by your monthly income. The result is your debt to income ratio

For instance, if you have a monthly debt of $5,000 and a monthly income of $20,000, your debt-to-income ratio is 25%. The highest debt-to-income ratio you should have is 36%, and a debt-to-income ratio of 20% is considered very good.

If you have a very high debt-to-income ratio, be very careful of lenders that want to offer you a loan. Be sure that they aren’t charging you exorbitant fees to cover any risk that you may default.

Gather the information you’ll need

You’ll most likely be faster with your personal loan application if you collect all the documents you have to provide. It will help you provide answers to questions faster and it means that you’ll have everything in one place when the time comes to send in your documents. You’ll generally have to provide:

- Proof of identity

- Proof of income

- Documentation about your existing debts

- Proof of employment

- Your mortgage and homeownership papers

A loan provider that doesn’t ask to see your supporting documents is not to be seen as credible.

Apply for a pre-approved offer

A lot of loan providers give you the chance to apply for a pre-approved loan offer. This generally includes a soft credit check, which doesn’t reflect on your credit score, rather than a hard credit check.

Although this is not a guarantee of your final loan terms, it will give you a good indication of the rates and terms you’ll likely get from each lender. The process of applying for a pre-approved loan offer also affords you an opportunity to see if the lender is helpful and supportive during the process.

Make sure You Read the Fine Print

Take your time to read the details very well before you choose one of the best personal loan companies. Some loan companies have hidden fees, like origination fees, which add to the overall cost of your loan. Others have prepayment penalties if you pay off the loan early, or one-off loan arrangement fees.

10 Dangerous Signs When Looking for a Reliable Loan Provider

It is quite unfortunate that not all lenders can be trusted. Be on look out for any of these red flags. If you find any of them, it’s a good sign to steer clear:

- Inexplicable high-interest rates. When you review some lenders for the same loan amount and repayment term, you might see that one set of interest rates is noticeably higher than the others.

- Inexplicable low rates. Though it may seem odd, very low rates can also be a red flag. If the interest rates stated don’t seem to rhyme with the general average, it could be a signal that the lender makes up the difference with a lot of hidden fees

- Unclear loan costs. If the lender isn’t clear about the cost of the loan, it’s an obvious sign that they are hiding something.

- No background checks on your ability to pay off the loan. If the loan provider doesn’t run a credit check and certifies that you’re able to repay the loan, it’s a clear sign that they intend to cover their risk with extremely high fees and rates.

- Bad customer reviews or unresolved complaints from customers. If many people complain about the same thing, then it’s a clear red flag.

- High-pressure sales. This is a case when the loan provider advises you to borrow more than you originally wanted to.

- Interest rates that are not monthly. Loan providers that have high rates and fees mostly likely hide them by quoting their interest rates per week or per day, instead of per month so that the rates would appear to be lower than they really are.

- If they demand access to your bank account. Most lenders give you the choice of linking your bank account so that you can make automatic payments. But a dangerous lender may insist that you give them access to your account, and then make extra withdrawals that force you to pay overdraft fees.

- They aren’t licensed in your state. Trustworthy loan providers will let you know the states they’re licensed in, and will not offer loans to people in states where they aren’t licensed. Credible lenders don’t hide this sort of information, but if you’re not sure about their license, there’s another way to find this out. Most lenders are registered through the state’s attorney general’s office.

- Unnecessary adverts and promotions. Trusted lenders reach their customers through the internet or adverts in conventional media. If a lender reaches out to you in a way that seems tricky, then it probably is tricky. Credible loan providers don’t offer loans by SMS or through the mail, and they do not come to your house without warning.

7. What are the differences between secured and unsecured Loans?

Secured Loans

The Benefits: Using a secured loan, you can give an asset to the bank as collateral. What this means is that if you don’t repay the loan, the bank can take control of the property that you gave.

Due to the fact that the bank knows that it has that choice, it sees a secured loan as a safe investment, which makes secured loans much easier to get, and also makes them readily available with lower interest rates than unsecured loans.

The major disadvantage is the risk that happens if you can’t repay the loan which is you losing the property that you gave as collateral.

The Drawbacks: Secured loans can be useful in making huge payments, such as a home equity loan. It is also useful for loans involving smaller payments over time, such as a mortgage or when refinancing. In addition to having lesser interest rates, secured loans most times have longer repayment periods and higher borrowing limits than unsecured ones.

Unsecured Loans

The Benefits: An unsecured loan is a type of loan for which you don’t offer property as a backup that the bank can take if you don’t repay them. Unsecured loans may be used for various reasons, which include student loans and personal expenses. This type of loan is often best for borrowers who don’t have sizeable assets, such as a home or a car, that they can give up as collateral.

The Drawbacks: Due to fact that this type of loan is a lot riskier for the banks, an unsecured loan often comes with a much higher interest rate, plus a lower borrowing limit and a smaller repayment period. When you’re being considered for such a loan, the banks will review your personal credit score to see if you’re eligible, so get ready to show your credit score.

8. Which is better between personal loans and credit cards?

Just like most of the financial decisions made by a consumer, there is really no right answer to this question.

Both personal loans and credit cards have strong merits and demerits, which are cost vs ease. If the ease of swiping a card and having a product magically appear at your doorstep is what’s more beneficial to you, then a credit card is your best option.

However, if you want to prevent overspending, then a personal loan is the better option. Personal loans usually have lower interest rates than credit cards, so they can be a very advisable means of reducing expenses that you know you can pay off quickly.

The average personal loan rate is around 10% but that can drop to 3-4% for borrowers with strong credit.

On the other hand, the average credit card has 19% interest for new customers, and 15% is considered a good rate.

Whether or not you go for a personal loan or credit, always remember to review a few providers before signing up. Everyone knows comparison shopping is the best way to select great deals from retailers during the holidays.

The same thing works for personal loans and credit cards: comparison shopping is the best way to see low rates, flexible repayment terms, and great introductory offers.

9. How is a credit score calculated?

Your credit score is calculated by taking into account your loan repayment history, credit card usage, and other financial signals that can give loan providers a rough map of how responsible you’re with money and how much of a default risk you are.

Despite what your credit score is, you can always find one of the best personal loan companies that will offer you a loan.

10. How do interest rates work?

The rate of interest means how much the loan provider charges a customer for a loan and it is calculated as a percentage of the amount borrowed. For instance, if you take out a loan for $50,000 with an interest rate of 10%, you’ll end up paying $55,000 overtime.

If you get an interest rate of 20% though, you’ll be paying $60,000. If you’re consolidating debt and the interest rate is still lower than your earlier loan, then you’re in good condition.

11. What is an APR?

An APR is a term for annual percentage rate. It adds the charges, fees, and payments to tell you the overall total of what your loan will cost you per year. The lesser the APR, the lesser you’re going to pay as time goes on.

To calculate the APR on a personal loan, it’ll vary depending on your loan provider, but it will definitely be lower than what you would receive from a payday or short-term loan. It typically starts from 10% and ends at 35.99%. It’s not proper to be in debt, but if you need a loan, then a personal loan could certainly be a better option.

12. How much can I get approved for?

There is no definite answer to this question, it’s all dependent on what you need, your income and your capacity. You have to be sure that the monthly payments aren’t a heavy burden on you. After all, it’s not wise to take a loan only to be unable to keep up with the payments.

13. What loan term should I take?

This is a really simple estimation, but what works best for you can’t be that simple. Should you decide to go for one of the best personal loan companies that give short-term loans, you’ll definitely have higher monthly payments but you’ll pay less interest over the duration of the loan.

If it’s spread out over a longer loan period, your monthly payments will be lesser, but the overall interest you pay will be much higher.

Conclusion

Whether you’re taking a personal loan to cover large expenses, or you’re doing so to consolidate your other debts, it’s important to check out various options so you will get the best rates out there.

This is why this guide is useful as it presents you with the best personal loan companies, the reasons for choosing them, and other helpful questions you might have. Hopefully, this will help you make the right financial decision.